Turkish deepsea import scrap prices are expected to remain relatively firm over the first quarter of 2023, supported by tight supply, posing a continued challenge to Turkish steel mill margins, sources said.

Platts assessed Turkish bulk imports of premium heavy melting scrap 1/2 (80:20) at $386.75/mt CFR Dec. 23, unchanged day on day.

The assessment averaged $444.69/mt CFR over the year to Dec. 23, down slightly from $463.43/mt CFR over 2021, despite the assessment also reaching an all-time high of $665/mt CFR March 16, as a result of raw material supply concerns fueled by the Russian invasion of Ukraine in late February.

The LME scrap forward curve over January-March 2023 is in a soft backwardation, with January contracts assessed by Platts at $381.50/mt Dec. 23, while March contracts were at $379.50/mt. This suggests future traders expect some softening in physical prices in the near term, but prices are expected to remain largely firm.

Scrap availability has remained tight amid lower industrial activity and weak consumer confidence in the key ferrous scrap exporting regions to Turkey, such as the UK, continental Europe, the Baltics and the US. The usual seasonal downturn in scrap collection rates during the winter has also hit supply.

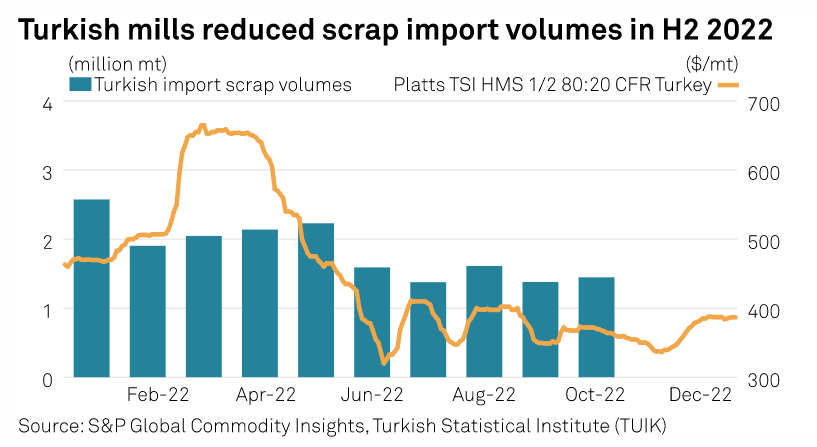

Turkish mills struggled to remain competitive in the export steel markets into the second half of 2022, relying mostly on domestic steel demand, amid rising production costs caused by sharp hikes in electricity and gas prices, as well as relatively firm scrap prices.

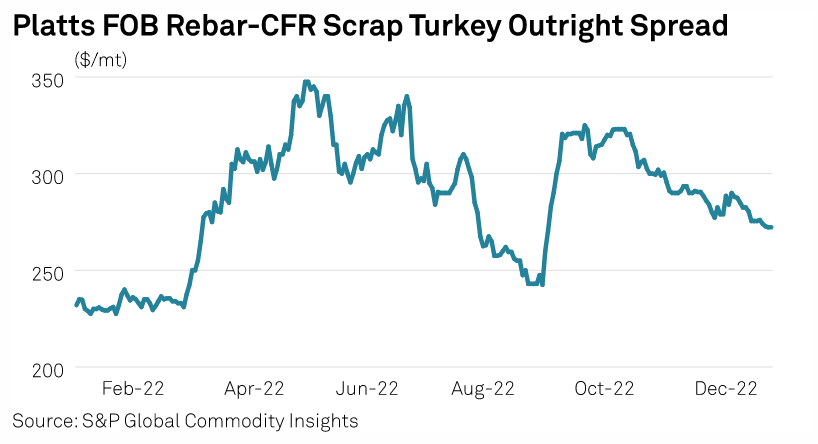

Platts, part of S&P Global Commodity Insights, assessed the daily outright spread between Turkish export rebar and import scrap at $272.25/mt Dec. 23, reaching at its lowest level since early September. Mills had previously attempted to target an outright spread of around $300/mt to factor in higher scrap and production costs but have had to accept a lower spread to catch sales in the export rebar market.

Platts assessed Turkish export rebar at $659/mt FOB Turkey Dec. 23, unchanged day on day.

In September, Turkish electricity prices rose 50%, and gas prices for industrial use also rose 50.8%, while in October, gas prices rose around 37.2% for industrial use. So far, market sources aren’t expecting a further increase in gas and electricity prices in January 2023.

“Come January, the new minimum wage will start to weigh on mills’ costs, and margins are super squeezed already,” one Turkish scrap agent said, referring to Turkish President Recep Tayyip Erdoğan’s announcement Dec. 22 of a 55% increase in the Turkish minimum wage to Lira 8,500 a month ($455), effective January 2023, in an attempt to ease the impact of rampant inflation on workers, ahead of presidential elections due to take place June 18.

“It is going to be challenging in 2023, but maybe before the elections, the government will give some [support] package to the industry,” a Turkish trader said. “I don’t expect the demand to be much lower than this year, and it will be difficult for Turkish mills stop production. The capacity utilization is already 50%-55%, which is supported by the domestic market, but for more capacity usage it needs to be better in the export market.”

Turkish market participants will also be looking closely at how competing scrap demand develops from India, the world’s second-largest crude steel producing nation after China, with ambitions to reach an annual crude steel production of 300 million mt by 2030.

India became a key competitor to Turkey for scrap in the second half of 2022, as high coal prices and high container freights (India is a large importer of containerized scrap) made bulk scrap cargoes more attractive pricewise.

According to S&P Global’s Commodities at Sea platform, India imported about 951,300 mt of ferrous scrap in 26 bulk cargoes since September 2022, with four further cargoes totaling 166,000 mt in transit as of Dec. 23.

Longer-term factors

Market participants will also be closely watching in January 2023 for the European Parliament’s plenary vote on the European Commission’s proposed legislation on waste shipment exports.

Under the proposal, EU ferrous scrap exports to non-OECD countries will only be allowed if they can be managed sustainably. The time frame for implementation is unclear, but market sources have previously voiced expectations of 2026.

The EU is the world’s largest exporter of ferrous scrap, with 2021 total export of ferrous metals scrap reaching 19.5 million mt, according to Eurostat data.

Turkey, an OECD member, could theoretically benefit in terms of reduced competition for material, should the legislation be approved in its current guise. India, a non-OECD member, but a growing scrap importer, could be affected.

Increased demand for ferrous scrap globally, and thus greater competition for import-reliant Turkey, is likely to continue in 2023, as steel mills globally look to introduce a greater volume of ferrous scrap into their raw materials mix as a part of a strategy to reduce carbon emissions from production.

As EU sanctions on Russian crude and oil products come into force, the Baltic and Black Sea shipping markets face uncertainty.

In this episode of the Platts Commodities Focus podcast, our EMEA Tanker Editors and Freight Analytics team delve into the challenges and opportunities facing shipowners in these regions. From navigating new strategies to considering the potential impact of these sanctions, join us as we explore what the future holds for shipping in the west.

Post time: Dec-30-2022