This report is part of the S&P Global Commodity Insights’ Metals Trade Review series, where we dig through datasets and digest some of the key trends in iron ore, metallurgical coal, copper , alumina, cobalt , lithium , and steel and scrap . We also explore what the next few months could bring, from supply and demand shifts, to new arbitrages, and to quality spread fluctuations.

Asian iron ore is likely to see a bearish third quarter on expectations of weak demand from steelmakers in China amid extreme weather and unfavorable production margins, while there is cautious optimism over the Chinese government announcing measures to support the troubled property market and potentially additional stimulus moving forward.

The Platts Iron Ore Index, or IODEX, was assessed at a wide range of $97.35-$122.4/dmt CFR China in Q2, showed data from S&P Global Commodity Insights. This reflected volatility in seaborne iron ore prices due to declining spot supply from miners and macroeconomic factors like interest rate hikes by the US Federal Reserve resulting in high financing costs.

Platts assessed 62% Fe IODEX at $97.35/dmt CFR North China May 24, a six-month low, before prices recovered to $111.6/dmt CFR China June 30, still down 12% from the end of Q1, S&P Global data showed. The assessment for the index stood at $107.6/dmt July 11, and mills are now unlikely to increase their demand for iron ore further in Q3 unless they see clearer signs of steel demand returning to levels that can support healthy production margins.

Trading volumes of medium-grade fines

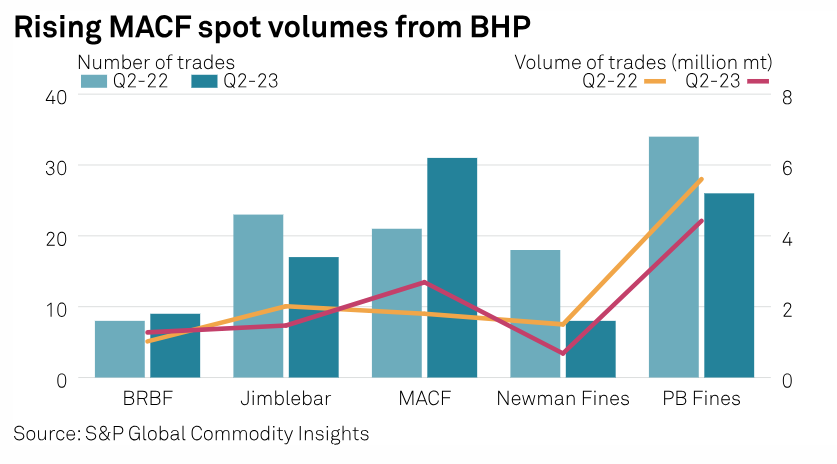

The total number of spot transactions for mainstream medium-grade fines cargoes by major miners BHP, Rio Tinto and Vale fell 13% year on year in Q2, S&P Global data showed.

Rio Tinto reduced spot volumes of Pilbara Blend Fines in Q2 but increased volumes in its long-term contracts, composed mostly of brands other than PBF, according to market participants.

The major increase in supply came from BHP’s MAC Fines, whose spot volumes over the quarter rose 49% year on year as the company’s South Flank project in Western Australia slowly replaces output from the Yandi mine, which is nearing the end of its life.

Both BHP and Rio Tinto were not immediately available to comment on their supply trends in Q2.

Low Brazilian high-grade fines demand

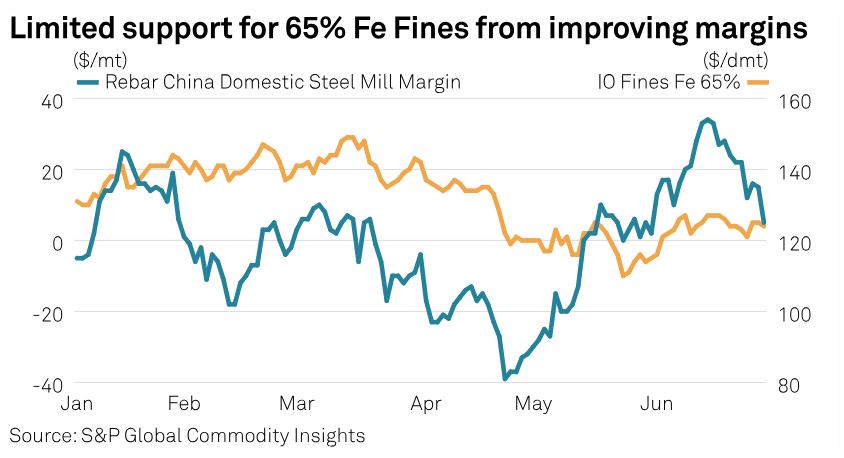

Demand for Brazilian high-grade fines was lackluster in Q2, although steel production margins gradually increased from late April before turning positive mid-May due to a fall in feedstock coke prices. Most steel mills in China continued to prioritize using low and medium-grade fines during this period given the risk of a rapid erosion of margins amid decreasing steel prices.

The supply of Vale’s Carajas Fines ramped up in Q2, when eight spot cargoes were sold by the mine, compared with seven in the same period last year, S&P Global data showed. The total volume traded rose 23% to 1.2 million mt over the same period, which indicated a rise in supply.

However, mill sources said that blending economics over this period was only favorable when they used the medium-grade fines as feedstock, which put pressure on the high-grade fines prices.

Platts assessed 62% Fe IODEX at $106.8/dmt, 58% Fe at $90.65/dmt and 65% Fe at $121.8/dmt on April 24, all on CFR North China basis, showed S&P Global data.

Spike in NBL supply

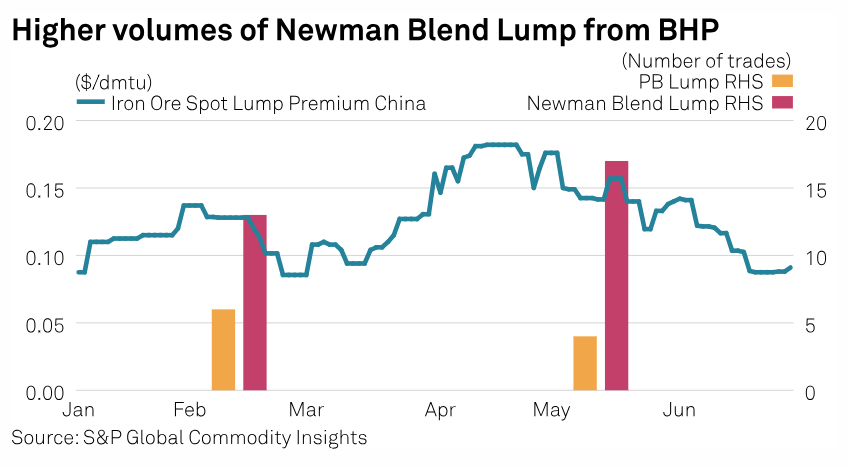

There were 21 spot transactions for lump cargoes by BHP and Rio Tinto in Q2, up 11% quarter on quarter, S&P Global data showed. Among these cargoes, BHP sold 17 cargoes of Newman Blend Lump, up 31% from Q1 2023.

Lump premiums spiked over April due to an upward trend in steel production margins amid higher coking coal supply from Australia, which in turn reduced the price of coke and made it cheaper to remove contaminants in lump. Sintering cuts in northern China also offered support for lump demand over this period.

Any increase in lump premiums in Q3 will depend on the pace and strength of recovery in both infrastructure and property markets in China. The country will extend two financial policies supporting the stable and healthy development of the real estate market to the end of 2024, according to a notice released by the People’s Bank of China and the National Administration of Financial Regulation July 10.

Participants said that direct charge materials, such as lump and pellets, could see some support from these measures and if they lead to steel production margins remaining positive, steel mills in China would likely maintain high operation rates in Q3.

BHP raised its lump spot sales volume amid Chinese sintering cuts as mills in the country pivoted towards direct charge metals as feedstock, eventually pressuring seaborne spot lump premiums, according to an S&P Global survey of market participants. Lump premiums fell to a four-month low of 8.7 cents/dmtu June 21.

Ample availability of pellet supply portside in China also drew the demand of mills away from direct charge ore in June. The pockets of sintering reductions in the country were reportedly short-lived and therefore had a limited impact on mills’ appetite for sinter feed. With IODEX hovering at around $110/dmt CFR China in June, it was less lucrative for mills to pay additional premiums to secure lump cargoes of higher iron content, capping demand potential for direct feed.

India-based pellet sellers continued to prioritize their domestic market in Q2 amid difficulty finding export avenues. They also cut production to better balance margins and fundamentals amid sporadic seaborne buying interest.

Post time: Jul-20-2023