China’s monthly manufacturing steel demand rebounded in June but was still lower than a year ago, S&P Global Commodity Insights data showed. While construction-related manufacturing remained depressed, most of the other sectors showed improvement due to resilient exports and government support to infrastructure investment.

Several market participants expected manufacturing steel demand outside of property-related sectors to “fare well” for the rest of 2023. However, elevated steel production would continue to dent steelmakers’ steel profits.

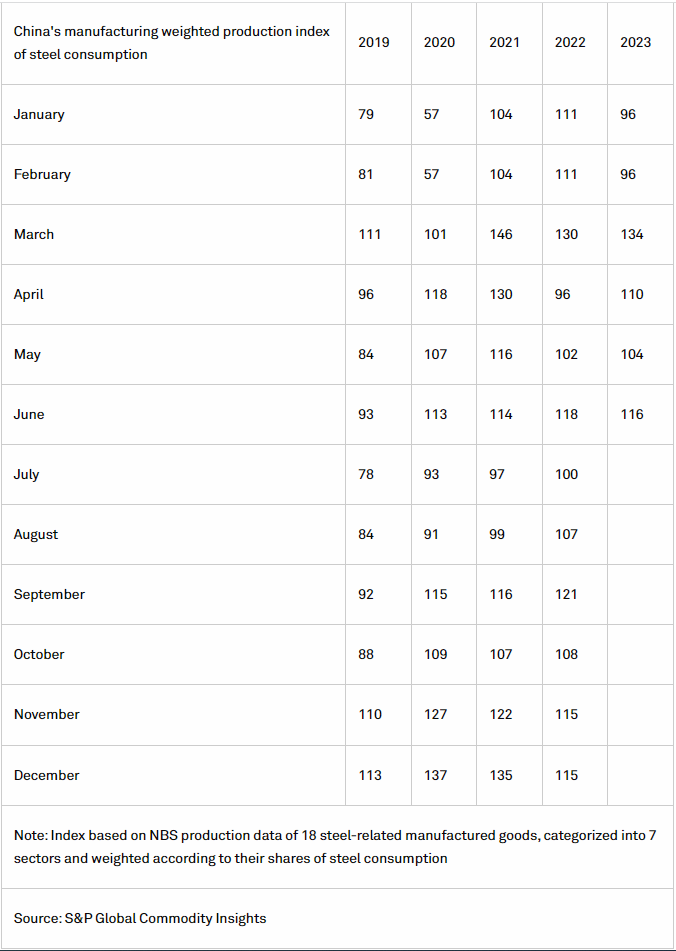

China’s manufacturing production index for steel consumption, produced by S&P Global, was at 116 points for June, up from 104 points in May, but still lower than the year-ago 118 points.

The production index is based on production data from China’s National Bureau of Statistics for 18 steel-related manufactured goods, categorized into seven sectors and weighted according to their share of steel consumption. The monthly production average in 2018 is used as the baseline of 100.

In June, manufacturing of vehicles, ships, home appliances, power generation facilities and railway facilities all posted month-on-month and year-on-year increases, but machineries and containers fell on a yearly basis, the NBS data showed.

China’s vehicle production, accounting for around 21% of the manufacturing steel demand, has been on an upward trend ever since March, due to strong exports.

China’s vehicle exports in June increased 65.7% on the year to 411,000 units, taking exports in the first half of 2023 to 2.341 million units, up 77.1% on the year, according to China’s customs data.

Owing to the strong exports, especially for electric vehicle cars, China’s vehicle output in June still increased 0.8% on the year to 2.564 million units despite sluggish domestic demand, the NBS data showed.

“China’s passenger car production and its steel demand are expected to continue upwards in the second half of 2023, thanks to robust exports. But the improvement in home appliances may not be sustainable due to dismal sales of new homes,” a mill source said.

Meanwhile, some market participants said steel demand from shipbuilding will remain strong for the remainder of this year due to the large backlog of shipbuilding orders received in the past few years, while China’s fiscal support to infrastructure will continue to benefit power generation and transport related manufacturing sectors.

The biggest drag on manufacturing continues to be the property sector.

China’s production of excavators, an indicator of construction-related machineries, fell 15.3% on the year in June, according to the NBS data. The excavator output in the first half of 2023 was 18% lower than in the same period of 2022.

“I think China’s property sector has not yet hit the bottom, so the adverse impact on construction and manufacturing steel demand will not abate at least in 2023,” one eastern China-based trader said.

Given the dent to the property sector, China’s manufacturing sector was unlikely to generate much incremental steel demand for 2023, market sources said. They added that the profit margins of flat steel products, consumed mainly in manufacturing sectors, were unlikely to improve in the second half of 2023 should China fail to keep its crude steel output within 2022 levels.

The Chinese domestic hot rolled coil sales profit margin, an indicator for the flat steel market, fluctuated from Platts-assessed minus $12.03/mt at the start of 2023 to $26.13/mt mid-June, before falling to $7.78/mt on July 20, S&P Global data showed.

Post time: Jul-25-2023