The world heaved a sigh of relief when Beijing announced Nov. 11 new measures to relax its COVID-19 restrictions, while keeping China’s zero-COVID policy in place, and when Guangzhou on Nov. 30 revealed plans to remove most movement controls and resume public transport, among other new measures.

But China’s three main economic drivers – consumption, investment and exports – are still facing headwinds. How will the country achieve a breakthrough in growth?

Changes in China’s COVID-19 restrictions are insufficient to effectively stimulate short-term commodity demand at Asia’s top consumer, said Sijia Sun, an analyst with S&P Global Commodity Insights.

“The relaxation would cause the number of COVID cases to surge in winter, a peak season for COVID-19 to spread, leading to more scattered lockdowns or movement controls within the zero-COVID policy,” Sun said.

On Nov. 27, new COVID-19 cases in China hit a fresh high of 40,052, according to the National Health Commission, with more and more scattered lockdowns and “suggestions” on movement restrictions.

The number of new cases was higher than the peak recorded in April at about 28,000 new cases, when Shanghai was locked down. The total area currently in lockdown across China could widen further than the area affected in the second quarter, as the number of new cases has been rising drastically since the start of November.

Even when China managed to keep new COVID cases on very low levels in October, recovery proved difficult for the country’s consumption sector. China’s Q2 GDP growth was 0.4%, down from 4.8% in Q1.

Sun is expecting a real demand recovery to most likely happen in March, when the political reshuffling at the National People’s Congress is completed, and after the Lunar New Year celebrations are over.

Speaking of celebrations, China’s National Day Holidays from Oct. 1 to 7, also known as the Golden Week, are one of the most sought-after breaks during the year. For market observers, it serves as a good economic indicator.

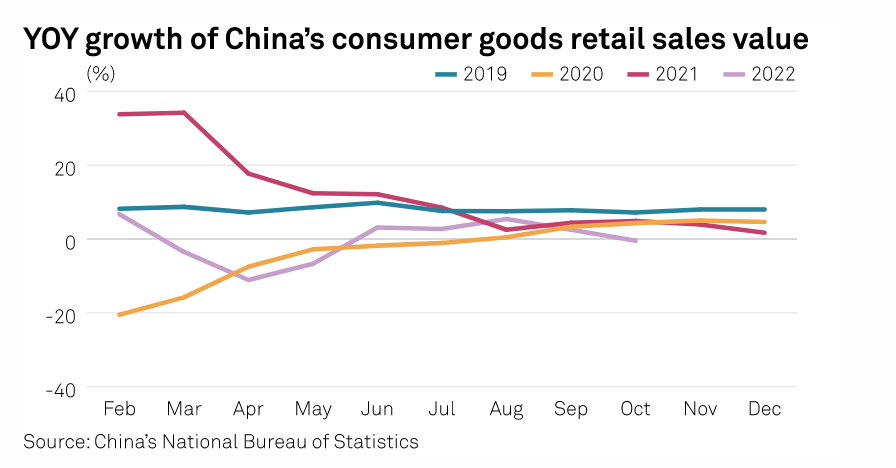

But during the recent Golden Week, the number of domestic trips were down 18% on the year and were about 40% lower than in the same period in 2019, due to a resurgence in COVID-19 cases. Poor tourism numbers signal China’s difficulties in consumer demand recovery under the country’s long-standing zero-COVID policy.

The widespread COVID resurgence in November will weigh further on the already weak consumer demand.

Liang Wannian, head of the National Health Commission’s Leading Group for Epidemic Response and Disposal, said Oct. 12 that there is no timetable for lifting China’s zero-COVID policy, adding that the death toll would be too large if social restrictions are lifted.

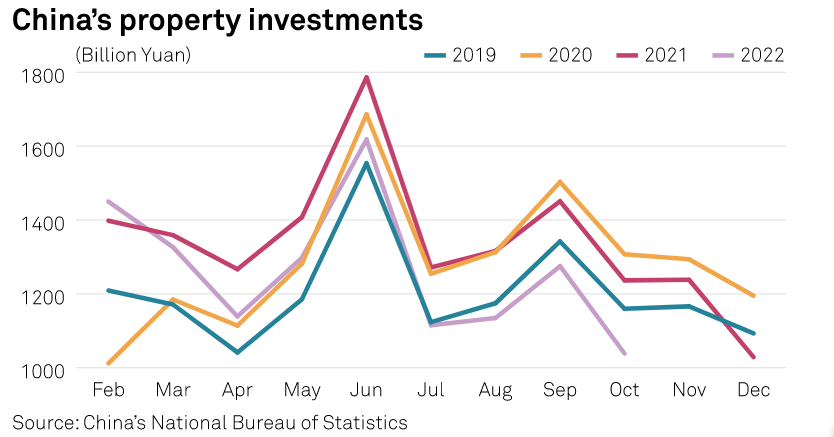

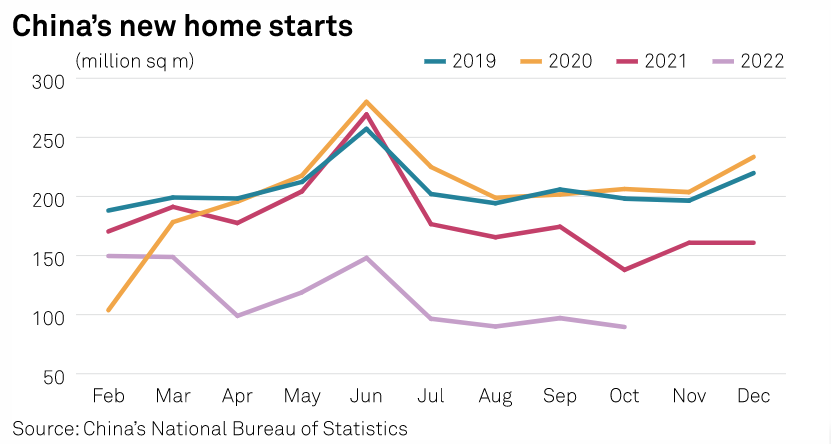

Apart from the sluggish domestic consumption, China’s property debt crunch has been adding extra pressure on the economy, with investments in the sector slowing to the worst levels in 30 years.

China’s property sales are likely to have an “L-shape” recovery in 2023 given the government’s efforts to boost the sector. But any major upturn is unlikely in the foreseeable future as buyers’ confidence remains weak due to stagnant household income caused by the pandemic resurgence and developers’ debt crunch.

Meanwhile, the growth in China’s overall exports is expected to slow further in late 2022 and H1 2023, amid rising interest rate hikes in the US and the growing energy crisis in Europe.

The export value of Chinese machineries in dollar terms decreased 7.1% on the month and 0.7% on the year in October, China’s customs data showed. The year-on-year growth in the machinery export value has fallen sharply ever since the start of 2022, all the way down from a 18.2% year-on-year increase seen in December of 2021.

The Shanghai securities composite index has dropped 22% from late 2021 to October, showing a lack of confidence in the market as investors see no effective method has been implemented so far to bring the economic growth back to a reasonable pace.

Readjusting carbon reduction ambition

Feeling the pressure of a slowing economic growth, it is clear is that China is now rebalancing its carbon reduction ambitions.

Against this backdrop, Beijing has taken a U-turn in its petroleum import and export policy to boost economy by encouraging international trade.

Since the second half of 2021, the government cut clean oil product export quotas to reduce high-carbon product outflows to meet its net-zero target. China imports more than 70% of its crude supply, and as crude prices rallied amid the Russia-Ukraine war, Beijing had further tightened its policy to keep clean(?) products at home to ensure domestic supply and fight against inflation.

Even when gasoline and gasoil export margins in June went beyond $30/b and $40/b, respectively, the domestic demand recovery was slow due to the zero-COVID policy. China’s clean product exports fell in JUNE? to a seven-year low of 1.58 million mt, or 426,000 b/d.

With a 40.2% year-on-year reduction in the product export quota allocation by end-August, China’s combined key oil product exports slumped 47.5% to 16.35 million mt over January-August from the same period in 2021, customs data showed.

With no signs from the government to relax quotas and COVID controls until September, analysts further lowered forecasts on China’s GDP growth and oil product demand during the peak season.

But on Sept. 30, Beijing released 13.25 million mt of clean oil product export quota for the year. This raised the total quota allocation to 37.25 million mt for 2022, cutting the year-on-year quota reduction sharply from 40.2% to 1%.

Moreover, the government for the first time allowed quota holders to roll over their remaining 2022 quotas to 2023.

This suggested Beijing’s aim to encourage oil product exports by providing companies the flexibility and freedom to control their export volumes, in line with market fundamentals and sales margins, – a stark contrast to the government’s previous efforts of establishing strict controls.

In addition, the government also granted 21 refineries with 24% of their 2023 crude import quota in advance on Sept. 30, without precedent, in an effort to boost imports and the sector’s refining activity.

Some of these quota winners had struggled from tightened operations supervision since April 2021, resulting in four of them getting removed from the quota allocation list this year.

“The about-face moves indicated that the government is willing to adjust some of its long-term policy principles to stimulate the economy in a short term in order to continue with the zero-COVID controls,” a Beijing-based analyst said, adding that the Chinese government’s decision-making chain is shorter than most of the foreign countries, allowing sudden adjustment when necessary.

Slowing steel

China’s stance on cutting carbon emissions in the steel industry remains comparatively tough, as the government still eyes to cap the country’s 2022 crude steel output within 2021 levels.

The steel industry accounts for about 15% of China’s total carbon emissions.

However, in a bid to avoid further pressure on an already slowed economic growth, the government-mandated output cuts this quarter are likely to be much more modest compared to Q4 2021.

Some steel mill sources said if it were not for the economic slow down, the central government might have still sought to reduce 2022 crude steel output by over 50 million mt, or 5%, from 2021.

As of Nov. 24, China still hasn’t announced its goal for crude steel reduction for 2022. Some market participants said given the sharp slowdown in property steel demand, China’s crude steel output in 2022 should naturally decline from 2021 levels.

While China has yet to announce its crude steel reduction goal for 2022, market observers believe there will be a natural decline from 2021 levels due to the sharp slowdown in steel demand from the property sector.

Without stringent government-mandated output cut orders, China’s 2022 crude steel output is expected to drop by less than 20 million mt or even be just on par with 2021′s output of 1.035 billion mt.

Post time: Dec-05-2022