This report is part of the S&P Global Commodity Insights’ Metals Trade Review series, where we dig through datasets and digest some of the key trends in iron ore, metallurgical coal, copper, alumina, cobalt, lithium, and steel and scrap. We also explore what the next few months could bring, from supply and demand shifts, to new arbitrages, and to quality spread fluctuations.

Key stakeholders in Asian iron ore markets witnessed shifts in sintering feedstock preferences as the focal point revolved around margins, with seaborne prices expected to find firmer grips through the peak steel production season in the second quarter.

S&P Global Commodity Insights analysts forecast the Platts 62% Fe iron ore index, or IODEX, to average $120/mt CFR in 2023. The highest iron ore and steel prices of the year are expected to occur April-June, traditionally the strongest quarter due to resumption of construction activity in the Northern Hemisphere amid warmer weather.

Seaborne iron ore prices fluctuated within the $120-$130/dmt CFR China range through most of the first quarter. Market makers widely deemed the price span as acceptable, although the Q2 outlook also remains hinged on improvements in import margins as Chinese steel mills have borne the brunt of lukewarm sales so far in the year.

Tepid steel mill margins and weak downstream demand could temper iron ore price increases, according to S&P Global analysts.

Brazilian feedstock gains traction

Platts IODEX scaled to a nine-month high March 15 amid a flurry of trades seen for the IODEX basket of five iron ore fines brands. Demand and supply fundamentals for higher-Fe Brazilian fines found a firmer footing, leading to a wider 65%-62% Fe spread that showed a recovery in Chinese demand.

Demand for Brazilian fines was evident from a doubling in spot trading activity observed in Q1, with 14 cargoes of Vale’s Carajas Fines (IOCJ) compared with seven in Q1 2022.

The total volume traded rose 41% to 1.68 million mt from 1.19 million mt over the same period, a clear sign of buyers’ preference for the Brazilian material.

The wider 65%-62% Fe spread, indicating a strong appetite for high- over medium-grade fines as sintering feedstock, peaked to a nine-month high of $16/dmt on March 22.

A sturdy demand recovery for higher Fe fines from Brazil in Q1 amid decent mill margins, despite supply tightness for the material, reflected Chinese steel mills running their blast furnaces at high operating rates, in line with expectations of a demand improvement at the start of the year.

The delivered price of Brazilian Blend fines was above $130/dmt for most of Q1, hitting the quarter’s high at $139.30/dmt CFR China on March 15.

Sinter feedstock preferences around margins

Chinese demand for Australian low-to-medium grade fines was stronger in Q1 compared with a year ago. The flagship Rio Tinto’s Pilbara Blend Fines (PBF) and BHP’s Newman High-Grade Fines (NHGF), alongside lower iron content Jinbao fines, proved to be strong candidates for mills.

Trade volumes for the most liquid PBF doubled in Q1, with 88 cargo deals seen over this period compared with 44 in Q1 2022.

With 36% of the PBF deals and 57% of the NHGF deals in Q1 concluding in March, this coincided with a timing where steel margins showed signs of recovery and mills started to switch to an increased usage of medium-grade fines.

Jinbao fines that have a typical Fe content of 58%-59% saw higher volumes to 14 in Q1 from four in Q1 2022.

Conversely, trading activities for Jinbao fines clustered around the first two months of the year, having greater demand amid the margin crunch, with around 86% of deals changing hands when discussions around lackluster steel margins were more prevalent.

Import losses, meanwhile, acted as a counterweight with production volumes of other medium-grade fines like BHP’s Mining Area C Fines remaining low in Q1.

Fewer production volumes and availabilities seen for MACF have led to more demand for Jinbao fines, which was also reflective through the more-pronounced drop in trading activities for MACF. Volumes in Q1 were slashed by half to 16 trades compared with the year-ago quarter.

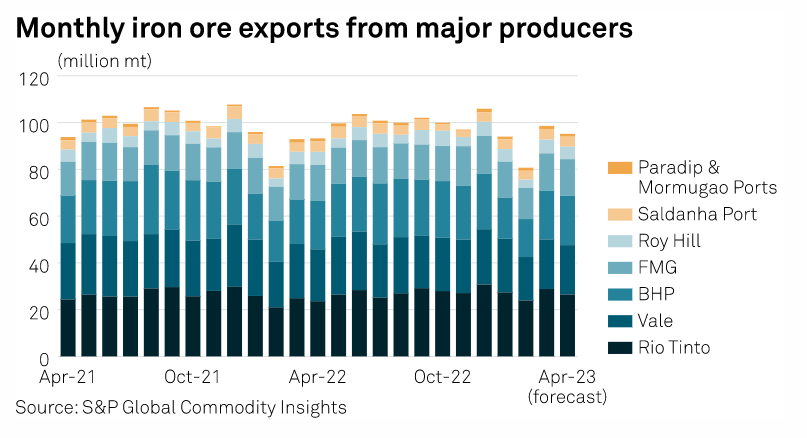

Overall, Australian exports are expected to remain resilient moving into Q2 and trading volumes are looking to tick up, with the April-June quarter being a traditionally strong demand season. The four largest Australian producers are expected to ship a combined 84.3 million mt in April, up from 82 million mt a year earlier, according to Platts cFlow ship and commodity tracking software from S&P Global.

Floating price trades continue to reign

Around 75% of deals in Q1 were done on a floating basis amid the macroeconomic volatility, as market makers with a lower risk appetite avoided taking outright positions due to the potential downside. This proportion of trades was a notch higher compared to around 68% in Q1 2022.

The recovery in steel margins despite a weaker-than-expected forecast of Chinese GDP growth for 2023, coupled with a short-lived period of five days where seaborne prices surpassed the $130/dmt mark in March, have showed somewhat resilient fundamentals. The momentum could spill over to the peak demand season in Q2 with further buy-side support expected to emerge in the iron ore market.

Post time: Apr-19-2023