China’s fast-rising steel production but slowly recovering end-user demand has continued to squeeze steel profit margins in April, with mills still showing no signs of cutting back on production. Mill sources said China’s steel capacity was too huge, but demand had more or less plateaued, and thus in order to retain market share, it was difficult for Chinese mills to voluntarily cut their production even when they were running at a loss.

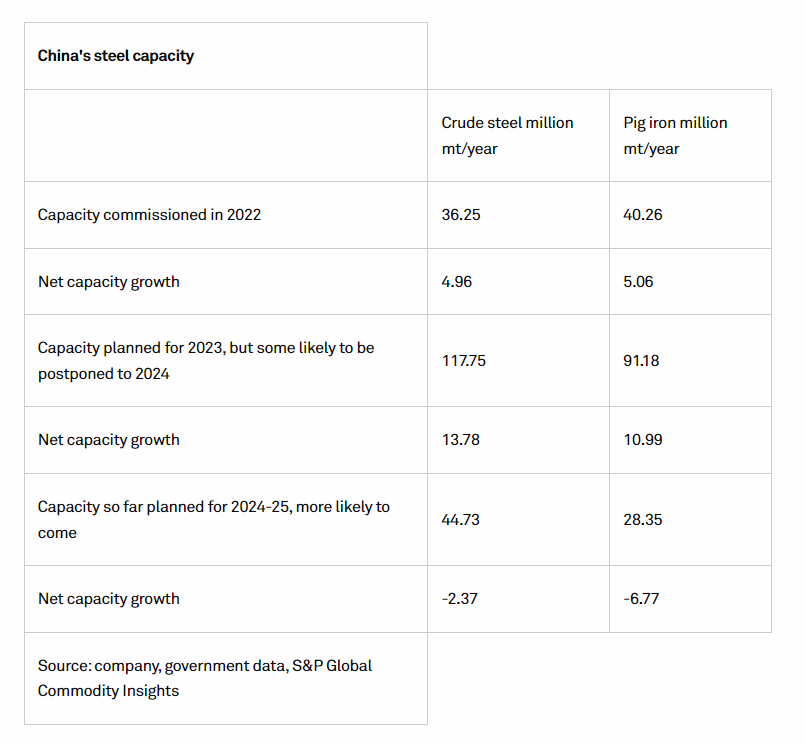

According to calculations of S&P Global Commodity Insights, China’s pig iron and crude steel capacity has been still marking a modest growth for 2023, as some of the replaced iron and steel making facilities were closed long time ago, mainly during 2017-2019.

Amid sluggish steel demand caused by slowdown in new home constructions and shrinking overseas demand for Chinese manufactured goods, whether any government-mandated steel output cuts could be implemented strictly would be crucial for the steel industry to contain steel output and maintain healthy profit margins for 2023, market participants said.

In 2023, Chinese steelmakers plan to bring up to 91 million mt/year of new pig iron capacity and 118 million mt/year of new crude steel capacity on stream through capacity swap mechanism, S&P Global data showed.

As some of the replaced facilities were closed during 2017-2019, for the year 2023, the commissioning of these new facilities will in theory lead to a net increase of 11 million mt/year pig iron and 14 million mt/year crude steel capacity, according to S&P Global calculations.

Some of these projects in 2023 may be postponed to 2024, should industry profit margins stay thin through 2023.

China’s pig iron and crude steel capacity are likely to decline slowly from around 2025, as most of the long-closed facilities will have been replaced by 2023 or 2024, and new capacity on stream in 2025 will be replacing facilities still in operation.

China’s capacity swap mechanism requires capacity of new facilities to be smaller than the replaced ones in order to reduce its overall iron and steel capacity.

However, China’s iron and steel capacity have been growing quickly ever since 2019, as either the replaced ones have already been closed long time ago, or the actual production capacity of new facilities are larger than their replaced ones.

As capacity swaps have done little in trimming China’s iron and steel capacity, the central government has directly required steel production cuts from 2021.

Steel output cuts

As of April 7, China’s National Development and Reform Commission was still soliciting opinions from major Chinese steel mills on details of the 2023 crude steel output cuts, according to some mill sources. Such output cut orders should be made soon, the sources added. Steel mills typically only receive verbal orders to cut output, sources said.

Previous media reports said China could announce a 2.5% cut to its 2023 output. Most market participants S&P Global spoke to expected a 2.5% cut might not be enough to fully offset the decline in steel demand, and thus its support to the steel prices could be limited.

“But even though the government-mandated output cuts for 2023 might be relatively small, considering the economic growth pressures, the announcement of output cuts should at least help to curb the current rapid growth in crude steel production and support market sentiments,” a mill source said.

Rising steel output

China’s daily pig iron and crude steel output over March 21-31 increased further to 2.451 million mt and 2.741 million mt, respectively, up 1.5% and 0.2% from the March 11-20 period, according to latest data of China Iron & Steel Association (CISA).

China’s daily pig iron and crude steel output in March were up by around 1.9% and 4.4% from the average in February at 2.41 million mt and 2.701 million mt, respectively.

CISA and the National Bureau of Statistics (NBS) have different statistical methods for China’s crude steel output, resulting in different output figures. But the trends in CISA’s steel production are usually the same as NBS.

Some market participants said daily pig iron and crude steel output surged further in early April, and the year-on-year growth rates of the pig iron and crude steel output in March and April should be about the same strength as in January-February.

China’s crude steel output in January-February increased by 5.6%, or almost 9 million mt, from the same period of 2022, NBS data showed.

In tandem with the rising steel output, the Chinese domestic rebar sales margin fell to negative $8.7/mt in average in late March and to negative $21/mt in early April, S&P Global data showed. The rebar sales margins in the same period of 2022 were $48.7/mt and $77.5/mt, respectively.

Post time: Apr-11-2023