The year started off on a bullish note for steel-making raw materials while the prices of finished products failed to exit the bear camp, casting a shadow on the margins of Asian steel mills.

“[Our] margins are squeezing. The current situation does not make sense as [raw material] costs are getting higher,” said a source from a major Japanese mill. “We used to have historically healthy margins but now it’s been hard.”

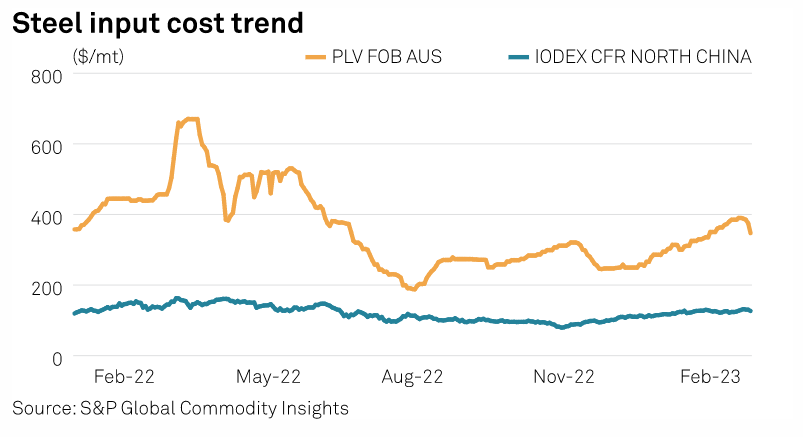

News on the Chinese property market’s recovery sent iron ore prices north earlier in 2023 while a supply crunch in Australia amid healthy seaborne appetite pushed up metallurgical coal prices.

The benchmark Platts Premium Low Vol, or PLV, price reached an eight-month high of $390/mt FOB Australia Feb. 17, according to data from Platts, part of S&P Global Commodity Insights. Similarly, benchmark Platts IODEX, reflecting the Asian seaborne iron ore price, also touched an eight-month high of $130.60/dmt CFR China Feb. 22. PLV and iron ore prices were assessed Feb. 28 at $347/mt FOB Australia and $124.10/dmt CFR North China levels, respectively.

It takes three months for raw material costs to be fully reflected in finished product prices, according to sources.

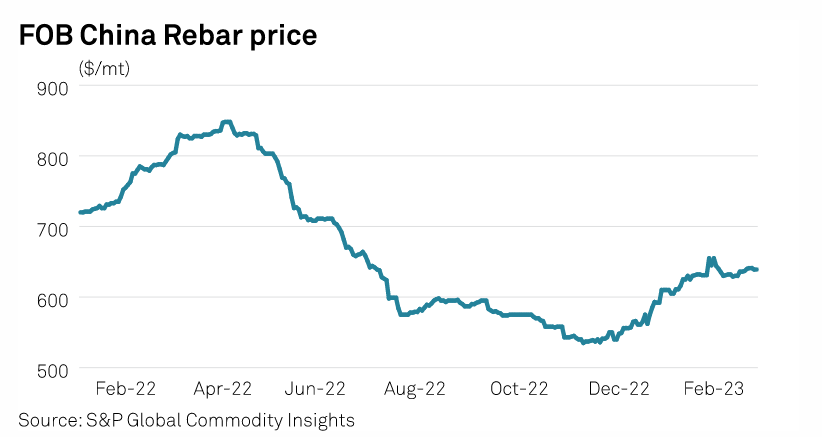

Spot prices of SS400 grade hot-rolled coil remained within $600-$670/mt FOB China levels between January and February while rebar hovered within $610-$640/mt FOB China levels over the same period.

Adding further to the steelmakers’ woes, commodity shipping rates have edged up amid a positive outlook for demand in March.

“[For] steel exports, we rely more on Handysizes. The ships we try to fix at $ 3,000/day couple of days back are now asking for $ 6,000-$ 7,000/day [for the week ended Feb. 20-24],” said a chartering manager of a major Asian steel mill, lamenting over the 50% surge in time charter rates for moving steels from east coast India to Southeast Asian destinations.

Bitter pill for buyers

Tracking the increase in raw material prices, major steel producers hiked their offer prices in February.

On Feb. 13, Vietnam’s local producer Formosa Ha Tinh Steel was heard to have raised offers for April/May shipment for HRC by $59/mt from the previous month to $694/mt CIF Vietnam, according to sources.

S&P Global reported Feb. 20 that Tokyo Steel hiked its March offer prices for all its rebar varieties by Yen 3,000/mt ($22/mt) with indications of further increases in the coming days.

JSW Steel hiked its domestic offer price for HRC twice in February with plans of another increase in March.

Buyers across Asia have had a hard time digesting the bitter pill of price hikes.

According to an Indonesian re-roller, offers from a Vietnamese mill were indicated at $765/mt CFR Jakarta levels for SAE 1006 grade and that would result in a selling price of $918/mt for cold-rolled coil. Another offer from a Japanese mill was heard coming at $785/mt CFR levels, which would result in CRC offers touching $938/mt levels.

Customers, however, remained unwilling to pay beyond $900/mt.

A major Japanese mill source said, “If it [input cost increase] continues we need to increase our prices which basically mills are now trying. If the market doesn’t accept, then mills may decrease the production to maintain the margin at a healthy level.”

Weak Chinese cues

Following China’s abandonment of its zero-COVID stance, Asian steel market participants were awaiting cues from the country’s government for clearer signs of price direction.

The seasonally adjusted General Composite Purchasing Manager’s Index improved slightly by 2.8 points on the month to 51.1 in January, according to data from Caixin.

Prices of iron ore and coking coal have remained high while finished steel prices have fallen by 2%-3% since the end of January. This has resulted in domestic HRC margins falling to minus $22/mt and rebar to minus $10.85/mt by February 7, according to S&P Global’s China mill margin model.

“We’ve seen a recent uptick in iron ore and steel prices on the back of positive China housing price data for January. However, we think the property sector will continue to be a drag on steel demand this year and see steel consumption from property down almost 6% on year,” said Paul Bartholomew, lead metals analyst at S&P Global.

“At this stage, we see China domestic rebar prices down 5% this year and hot-rolled coil down by 2.5%,” he added.

According to analysts at S&P Global, China’s crude steel production is expected to fall by 1.1% year on year to around 1 billion mt in 2023.

India striking a balance

The Indian outlook has been relatively positive compared to its Asian peers with New Delhi emphasizing on infrastructural development, which is expected to boost steel demand.

India’s finance ministry is raising the capital outlay for the steel sector for the financial year 2023-24, that starts April 1, by 21.5% on the year to Rupee 701.5 million ($8.8 million).

Domestic steel costs have also increased steadily as mills raised offer prices, although buyers have had a hard time accepting the price hikes.

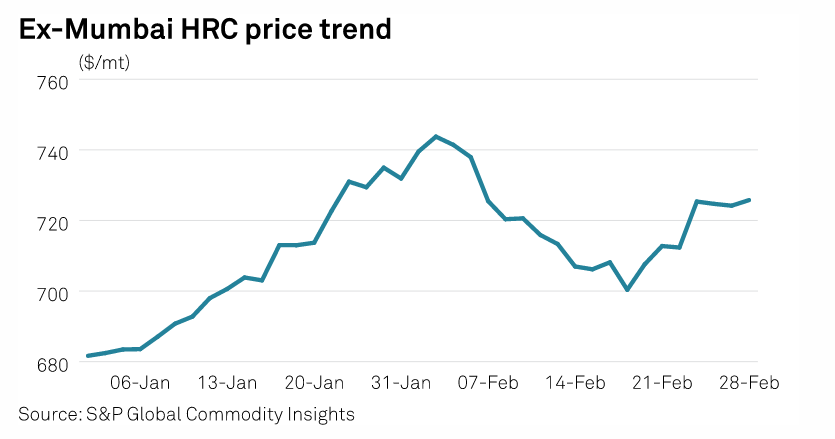

The price of domestic HRC increased from $680/mt ex-works Mumbai levels in January to $ 725.49/mt ex-works Mumbai Feb. 7, according to Platts data. India’s HRC increased from Rupees 56,500/mt basis ex-works Mumbai in the first week of January this year to Rupees 61,000/mt ex-works Mumbai levels on Feb. 6 and then softened to Rupee 60,000/mt ex-works Mumbai-levels on Feb. 28,according to Platts data.

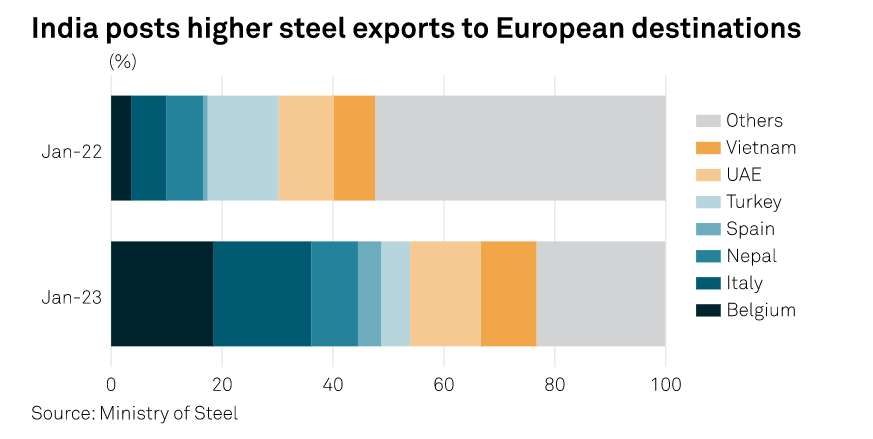

To offset the lower margins from domestic sales, steel mills in India have now been on the lookout for opportunities to export to Europe.

“Indian mills can manage their margins as they are getting better prices from exports to Europe now compared to their domestic prices,” an international trader said.

According to sources, deals concluded in February for base grade S235JR HRC were heard at $780/mt CFR Italy levels for April shipments.

Post time: Mar-07-2023